Blog & News

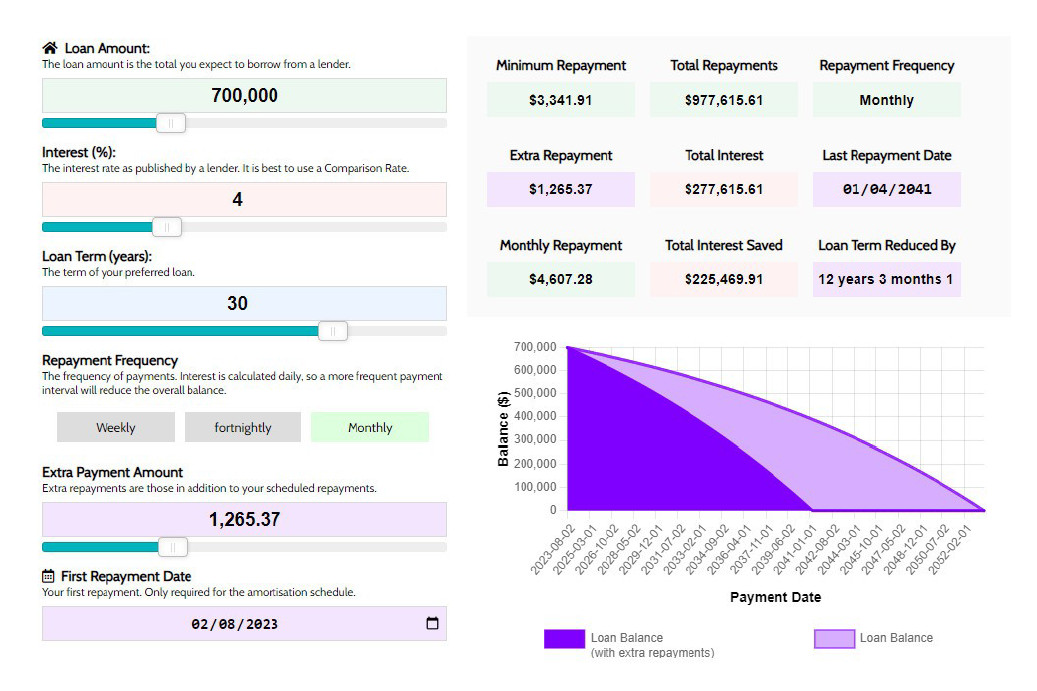

Let me let you in on one of the mortgage world’s worst-kept secrets: you can pay off your loan faster without changing your budget — if you switch to fortnightly repayments. Sounds like marketing spin, doesn’t it? But this strategy is not a gimmick. It’s simple math, and when done correctly, it can cut years off your loan and save you tens of thousands in interest. And yet, almost nobody understands how or why it works — or worse, they’re doing it wrong. Let’s fix that. The Psychology of Pay Cycles Most Australians get paid fortnightly. So the idea of synchronising your mortgage repayments with your income makes perfect sense. It feels more manageable. More frequent payments mean smaller bites. You don’t feel the sting of a big monthly debit, and your cash flow stays smoother. But that’s not the real advantage. The real power lies in what happens when you make 26 fortnightly payments per year instead of just 12 monthly payments. Let me explain. Let’s say you have: A $700,000 mortgage At an interest rate of 5.8% on a standard 30-year term. Your monthly repayment will be around $4,100. So over a year, you pay: 12 × $4,100…

Blog & News

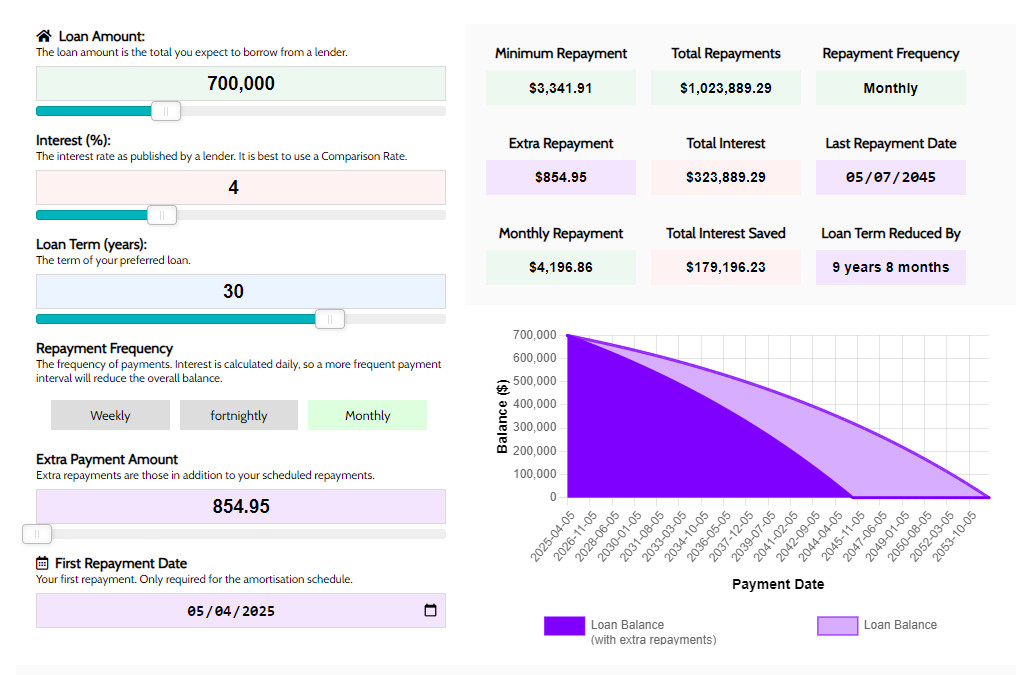

We’ve all heard the cliché: “Give up your daily coffee and you’ll own a home.” While it’s often delivered with a sanctimonious chuckle by economists in tailored suits, there is, beneath the snark, a kernel of unvarnished truth. The numbers don’t lie. And if you’re ready to walk with me — deep into the land of amortisation schedules, compound interest, and behavioural finance — I’ll show you how $5 a day (yes, just your modest piccolo or flat white) can demolish your mortgage term and rescue six figures of future interest from the bank’s grasp. Before we dive into spreadsheets, let’s touch on human behaviour. Psychologists call it the aggregation of marginal gains — small, daily improvements that, over time, snowball into life-altering results. Mortgage reduction is not a sprint, nor is it a single Herculean overpayment. It’s consistency that wins the war. $5 per day seems inconsequential — almost invisible. But multiply that by days, months, and years, and the effect becomes profound. Especially when pitted against the interest-compounding behemoth that is a standard 30-year home loan. Let’s construct a very common scenario: Loan Amount: $700,000 Interest Rate: 5.80% p.a. (variable) Loan Term: 30 years Repayments: Monthly Your minimum…

Blog & News

To suggest that there are only 14 or even 15 ways to pay off your home loan sooner is somewhat deceptive because countless factors can influence the duration and cost of your mortgage. However, this guide explores 30 comprehensive and actionable strategies—ranging from fundamental principles to advanced financial techniques—that will help you reduce your monthly obligations and shorten the term of your home loan. Beware of lenders bearing gifts. Many mortgage products offer an enticing introductory "honeymoon" interest rate—often significantly lower than the standard rate—only to revert to a much higher rate once the period ends. These deals may also include substantial exit fees if you attempt to refinance or pay off your loan early. Always calculate the long-term cost before committing to such a product. If the standard variable rate after the honeymoon period is above market rates, the initial discount may not be worth it. Learn more in our FAQ. A healthy habit is to assume a higher interest rate when making repayments. For example, if your home loan is at 4.00% per annum, set up automatic repayments based on a 5.00% rate. This builds a buffer for future rate increases and effectively reduces the loan principal faster,…

Blog & News

If you're new to the world of property ownership, you might be wondering what role a conveyancer plays in the buying and selling process. While it may seem like a straightforward transaction, transferring property ownership is a highly complex legal and financial procedure requiring meticulous attention to detail. This article provides an extensive examination of the conveyancing process, detailing the critical role of conveyancers, when you need one, what they do, and how they compare to solicitors. Whether you’re purchasing your first home, selling an investment property, or looking to understand the legal framework of property transfers. Conveyancing refers to the legal process of transferring property ownership from one party to another. This process involves a multitude of legal checks, financial calculations, and contractual obligations that must be met before settlement occurs. The transfer of land or property ownership is not as simple as exchanging money and signing a contract. Instead, it involves: Legal due diligence to confirm the legitimacy of the sale. Contract negotiation to define the terms and conditions of the transfer. Financial adjustments to ensure outstanding rates, taxes, and levies are accounted for. Settlement coordination to ensure the buyer gains clear and undisputed ownership. A conveyancer is…

Blog & News

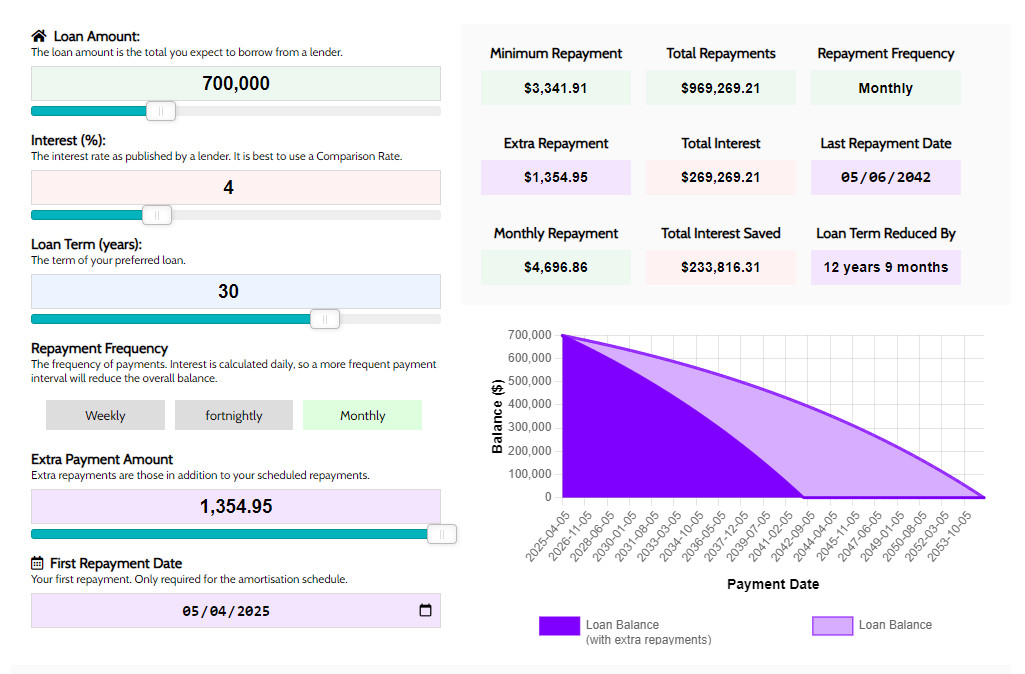

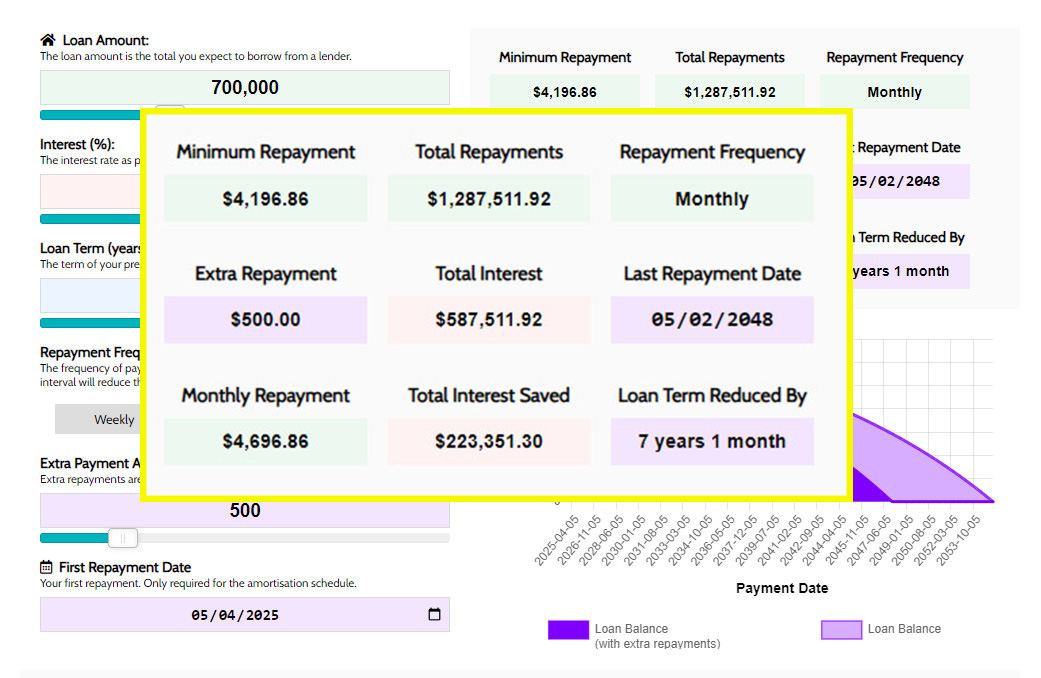

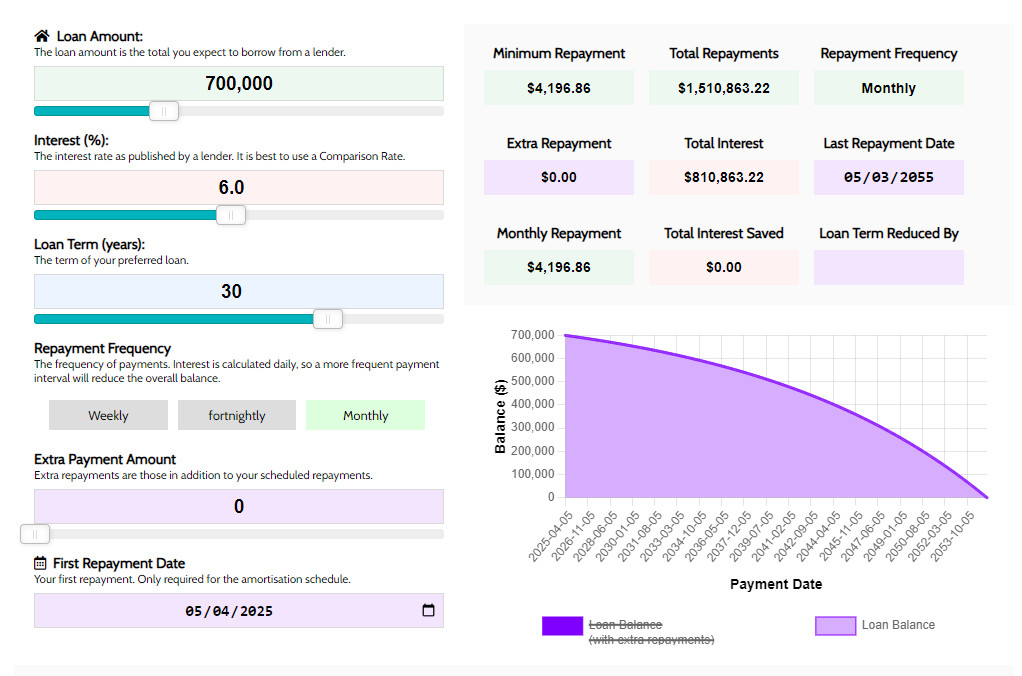

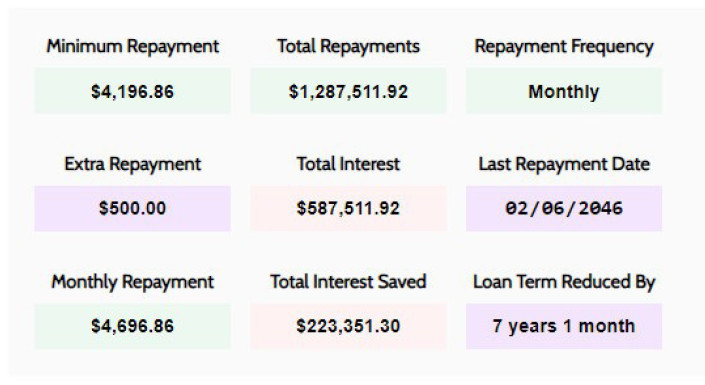

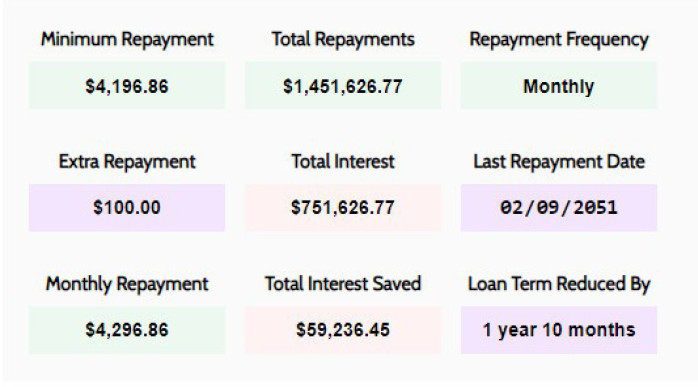

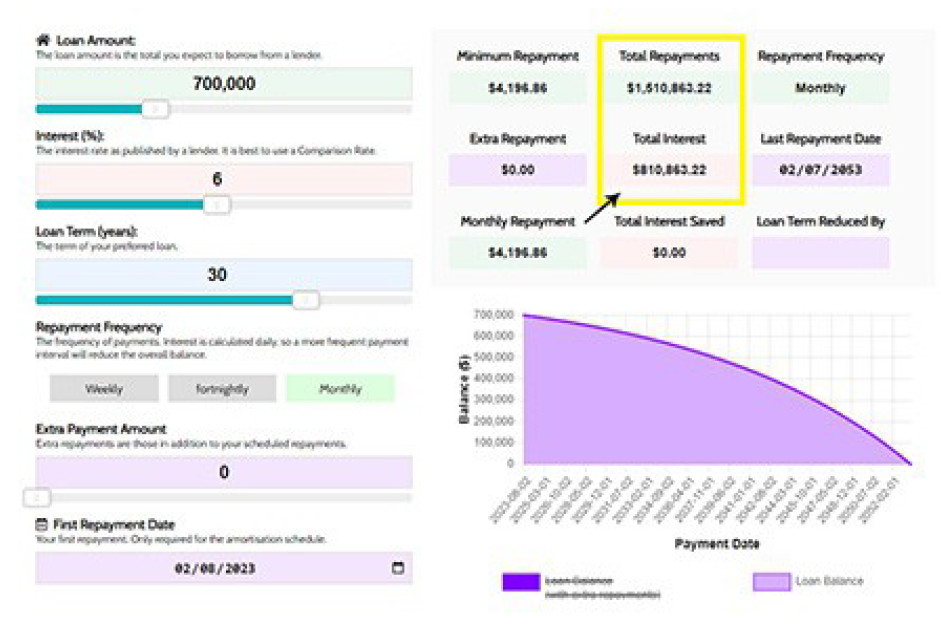

There’s a psychological trap buried in every interest rate cut — and it catches even the most diligent borrowers. The trap? The assumption that lower rates should equal lower repayments. On paper, that makes perfect sense. But if you’re serious about building wealth, minimising interest, and obliterating your mortgage timeline, this is the precise moment you double down. The following article focuses on the continuation of your current payment when rates drop. We understand that this is a privilege, and one that many cannot afford, so please understand that the strategy applies to those that are in a position to afford it right now. If you're encountering any measure of financial distress, you should first call us, but you should certainly plan on implementing the strategy when your circumstances improve. Remember, the benefit of extra repayments is that the funds are always available in an offset. Let’s unpack it with precision — and a little strategy. Take a $700,000 mortgage over 30 years. At an interest rate of 6%, your minimum monthly repayment is $4,196.86. Let's look at the impact of paying an extra $100 per month. Without a change in rate, but by simply paying an extra $100 into…

Blog & News

Stamp Duty — a term that strikes fear into the hearts of prospective homeowners, renters, and business owners alike. It is a tax that seems as ancient as the nation itself, lurking silently in the background, ready to pounce the moment a property transaction is on the horizon. Yet, like many of our beloved financial customs, its history is steeped in arcane mystery, laden with tales of bureaucracy, empire, and even rebellion. Let us embark upon an Australian odyssey, unravelling the origins, purpose, and persistent quirks of this often misunderstood levy. To begin with, let us turn our attention to the etymology of the term Stamp Duty, that beguiling phrase that marks, quite literally, the act of affixing a stamp to a document. The word "stamp" comes from the Old French estamper, meaning "to strike or impress", and the Latin stare, meaning "to stand" or "to be fixed." The stamp, which is the physical manifestation of duty, denotes an imprint of legality and obligation. But it was in the British Empire that the true birth of Stamp Duty occurred. As a colonial outpost of the British Crown, Australia inherited not only the penal code but also its fiscal frameworks, including…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}